This guest blog was written by David Rogerson, Director, Incyte Consulting Ltd. We will have a more detailed discussion of industry costs in our upcoming 2018 Affordability Report.

In its 2017 Affordability Report, A4AI found that the average price of 1GB prepaid mobile broadband, when expressed as a % of average per capita Gross National Income (GNI), varied between 0.84% in North America and 17.49% in Africa, with the majority of low and middle income countries surveyed failing to meet the 2% affordability target. Why?

At the most fundamental level, the affordability target can only be met either by increasing incomes or by reducing internet prices. While the income side of the equation is beyond the scope of this post, it is worth noting that incomes are likely to rise as a direct result of internet prices falling because better and greater use of the internet has the potential to boost productivity (albeit slowly). On the other side of the equation, if internet prices are excessive, they will fall once competition becomes effective so that prices are driven down to cost-based levels. But that still leaves one question: what are the costs (as distinct from the prices) of internet access?

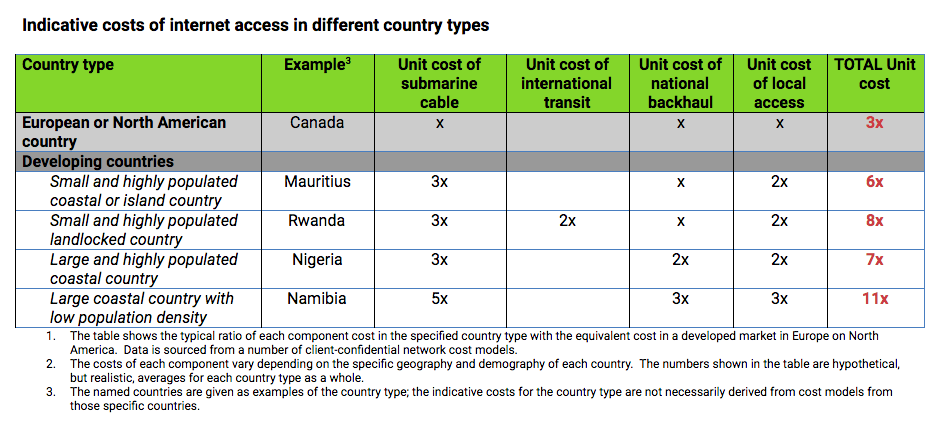

The costs of internet access can be broken down into four components:

- Local access: the fixed, mobile or WiFi connection to the national network.

- National backhaul: the link from the access point to the international gateway.

- International transit: In some instances, there is no immediate access to the an international gateway, such as with landlocked countries (and occasionally for others); in those cases there is a need to purchase capacity on another country’s network to reach the cable landing station.

- Submarine cable: investment in or lease of capacity from whichever of the submarine cables that lands in the country.

The key thing about almost all of these costs, and especially the last three categories, is that they are predominantly fixed costs: there is a sizeable up-front investment and a relatively small cost for incremental capacity. As a result, there are substantial economies of scale to be had, which means that small developing countries will inevitably suffer from higher unit costs which then typically lead to higher end-user prices.

One way to address this problem is to share infrastructure as much as possible with neighbouring countries. However, this is not an option available to island economies, and landlocked countries will always be at a disadvantage in negotiations with its neighbours, which control the essential facilities of transit and access to the cable landing station.

Another approach is to implement policies that stimulate demand — possibly going as far as explicit subsidies on retail internet access, both for infrastructure access and for end-user devices. Lower end-user prices provide the best way to stimulate demand. As volumes grow, unit costs will fall and further price cuts will be enabled. This is a strategy that should be adopted by all developing countries as they seek to improve internet affordability. However, it is important to notice that smaller and more isolated countries will always be at a disadvantage — no matter how good they are at demand stimulation, they will never achieve the scale available to economies elsewhere.

Similarly, the playing field is not level for all countries in terms of the network components necessary for internet access. Large countries with low population density will have a disproportionate cost in the national backbone network. Landlocked countries will have the additional costs of international transit, and they may struggle to avoid paying premium prices if they do not have a choice of transit providers. Island archipelagos have a slightly different problem in that they may require submarine cables to be installed within the country, thus increasing the cost of national backhaul.

Figure 1 illustrates the kind of exogenous cost differences that exist between countries. The table compares the cost components of internet access in developing countries with those in a typical European or North American economy. It is based on numerous cost models that Incyte Consulting has developed for national regulatory authorities in Africa, Asia-Pacific and the Caribbean. For simplicity, it is assumed that the unit costs (“x”) of the submarine cable, national backhaul and local access are all roughly the same in the developed country, and that the country has direct access to a submarine cable. For each of the developing country types, most, if not all, of the component costs will be higher. Using typical cost figures from a range of African countries, the extent of the cost variations is apparent: the costs may be up to five times those found in a typical European or North American country, even if all the same policies are followed and implemented with the same efficiency.

Clearly there is more work to do, and the internet in Africa remains expensive relative to income. However, while some high-capacity applications – such as interactive gaming and video – may not yet be affordable, the development and large scale adoption of lower-bandwidth applications is helping to drive internet use. In addition, innovation and policy initiatives in areas such e-Government, e-Health and the local caching of popular content. fuels demand, lowers unit costs, and results in prices that become ever more affordable. Positive feedback indeed!